Sequoia Capital — Four Numbers That Explain Why Facebook Acquired WhatsApp. Facebook buys Whatsapp for $19 billion: Value and Pricing Perspectives. This week, I was at the Tuck School of Business at Dartmouth, talking about the difference between price and value.

I built the presentation around two points that I have made in my posts before. The first is that there are two different processes at work in markets. There is the pricing process, where the price of an asset (stock, bond or real estate) is set by demand and supply, with all the factors (rational, irrational or just behavioral) that go with this process. The other is the value process where we attempt to attach a value to an asset based upon its fundamentals: cash flows, growth and risk. For shorthand, I will call those who play the pricing game “traders” and those who play the value game “investors”, with no moral judgments attached to either. The Investor/Value View I will start wearing my value cap, mostly because I feel more comfortable in it and partly because I understand it better. Value of equity = $19 billion The Trader (Pricing) View Closing Thoughts. The Social Conglomerate. When news of the Facebook/WhatsApp deal broke, a lot of people gave me credit for being prescient: after all, I had just written 1,568 words on why messaging was mobile’s killer app.

WhatsApp, though, was all but absent from the article, meriting but a single mention, and in parenthesis at that! Viber does have strong user numbers, claiming 280 million registered users and 100 million monthly active users, and that is certainly a big part of the battle, but the creation of a meaningful platform is a significant next step that Viber (and WhatsApp) has not taken. A platform is about multi-sided markets; LINE and WeChat are so valuable because they not only have the users, but also advertisers, commerce sites, and developers. Thus, while I’m skeptical of Rakuten and Viber, for LINE and WeChat the sky is the limit. Thus the reason for the exclusion: I believe that business models matter, and while WhatsApp had the users, I’d heard enough about their (admirable!) WhatsApp's Journey From Being Ignored To a $19 Billion Exit. Unless you've been living in a cave, you've probably heard that WhatsApp was purchased by Facebook for $16 billion in cash plus $3 billion in RSUs.

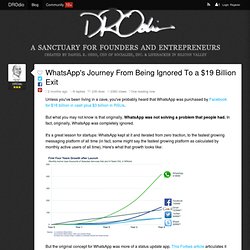

But what you may not know is that originally, WhatsApp was not solving a problem that people had. In fact, originally, WhatsApp was completely ignored. It's a great lesson for startups: WhatsApp kept at it and iterated from zero traction, to the fastest growing messaging platform of all time (in fact, some might say the fastest growing platform as calculated by monthly active users of all time). Here's what that growth looks like: But the original concept for WhatsApp was more of a status update app. “Jan was showing me his address book,” recalls Fishman. Even more revealing is this forum post that Jan, the CEO, wrote on the FlyerTalk forum back in May of 2009: But here's the kicker: Nobody responded to his post. "It appears that this requires the other party to also have the app installed, right?

" Ha! The best part of this story? Indeed. Price Per User For WhatsApp. Whatsapp and $19bn. Facebook just bought WhatsApp, paying $16bn in cash and stock ($4bn cash, $12bn stock at current prices) and $3bn in RSUs.

WhatsApp has 450m active users, of which 72% are active every day. It has just 32 engineers. And its users share 500m photos a day, which is almost certainly more than Facebook. This is interesting in all sorts of ways - it illustrates most of the key trends in consumer tech today in one deal. First, it shows the continued determination of Facebook to be the 'next' Facebook. Second, the winner-takes-all dynamics of social on the desktop web do not appear to apply on mobile, and if there are winner-takes-all dynamics for mobile social it's not yet clear what they are. Any smartphone app is just two taps away - a desktop site can crush a new competitor by adding it as a feature with a new menubar icon but on mobile there isn't room to do that.